As part of our ongoing commitment to strengthen the Care Navigation experience, plan members will now see Medical Second Opinion listed under Telemedicine on GreenShield+. This enhancement, introduced on January 1, directs members to a cobranded landing page where they can easily submit a request online. Members who prefer phone support can continue to reach Novus Health directly at 1‑855‑908‑1275 to speak with a Health Information Specialist.

What this means for plan members

Beginning January 1, 2026:

Get answers to your questions

Novus Health’s Medical Second Opinion Program can help you get answers to your questions, such as:

This transition strengthens the long‑term vision for Care Navigation and ensures members continue receiving trusted, high‑quality guidance when navigating important health decisions.

Women’s health evolves in meaningful ways from youth through later adulthood. Each life stage brings its own set of changes - physical, emotional, and hormonal - so in recognition of International Women’s Day on March 8, we’re highlighting the importance of awareness, proactive care and early support for women at every stage of life.

During their lifetime, women may experience shifts in menstrual health, reproductive needs, fertility, mental wellbeing, and later in life, the transition through perimenopause and menopause. Understanding these changes helps women make informed decisions and seek support that reflects their unique needs at each stage.

This month, we’re focusing on awareness around women’s health, with an emphasis on:

Every woman’s journey is different—but access to information, care, and supportive environments can make a significant difference in long-term health and quality of life.

By increasing awareness, we can create space for understanding, empowerment, and healthier outcomes for women at every age.

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

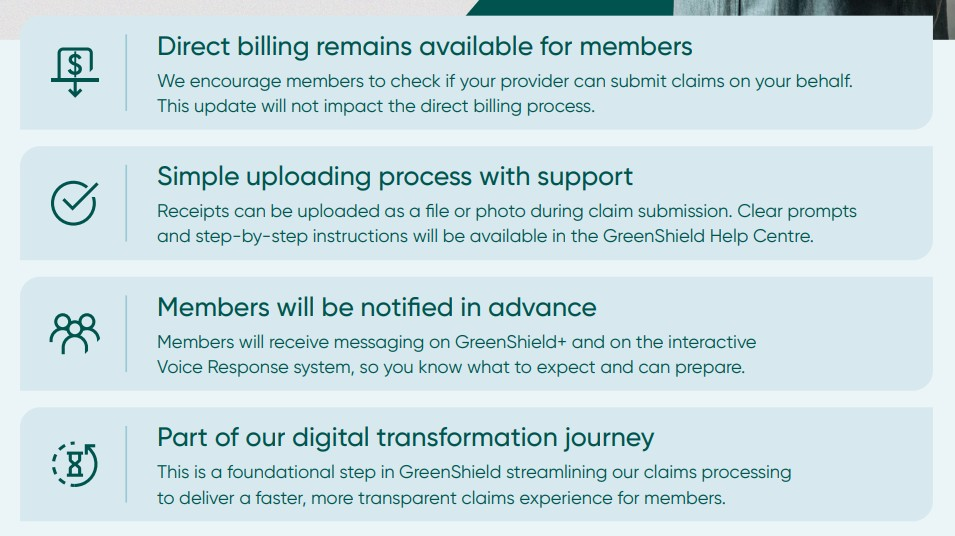

We previously shared that GreenShield would be moving to mandatory receipt uploads for all claims submitted through GreenShield+ starting March 4, 2026. GreenShield has now advised that this transition has been deferred, and there is no new implementation date at this time.

What this means for you:

You can keep submitting claims the same way through GreenShield+, just remember to hold on to your receipts in case they’re needed later.

If you have any questions, please feel free to reach out to the Benefits Team at Benefits@united-church.ca

Pension Awareness Day on February 19 is a reminder of how important it is to understand and make the most of your pension. Even if retirement feels far away, learning about your United Church pension plan and the benefits it provides can help you and your loved ones build a stronger financial future. The earlier you start planning and saving, the more prepared and comfortable you’ll be when life after work finally arrives!

The Power of Financial Literacy: What you need to know

Financial literacy is more than understanding money — it’s about feeling confident in the decisions that shape your future. Learning the basics now makes it much easier to build long-term financial security.

Know your retirement goals

Think about the lifestyle you want — compare what you spend today with what you might spend once you stop working.

Expect some costs to change — fewer work expenses, different priorities like travel or hobbies, and possible health-related costs.

Use simple planning tools — the Government of Canada’s Retirement Income Calculator can help you estimate future income and expenses.

Attend our Pension Information Seminar - learn about how the plan works, what it costs, what it provides, and how to apply for your pension when you're ready. The next session is February 19 starting at 1:00 p.m. EST.

Understand what shapes your retirement

Start saving now

The Bottom Line

Building financial literacy today sets you up for a more secure and fulfilling retirement tomorrow. Understanding your lifestyle, planning ahead, and using available tools can make a meaningful difference in your future comfort and confidence!

Thursday, February 19, 2026 | Starting at 1:00 p.m. ET / 10:00 a.m. PT

Click here for the start times in each of Canada’s Time Zones

The United Church of Canada provides a Defined Benefit Pension Plan for all employees who work more than 14 hours a week. Join us to learn about how the plan works, what it costs, what it provides, and how to apply for your pension when you're ready. In this program we'll describe:

Register here for the Zoom session!

If you have any questions, please contact Shenagh Rosa, Pension and Governance Advisor, at srosa@united-church.ca

February often brings attention to heart health, but it’s also the perfect moment to reflect on the powerful connection between your emotional wellbeing and your physical health. These two parts of your life don’t operate in isolation; they influence each other every day.

When stress, worry, or emotional strain builds up, your body often feels it too. Fatigue, tension, changes in sleep, and shifts in energy can all be signs that your emotional wellbeing needs attention. And the reverse is just as true - when your body feels strong and supported, your mind is better equipped to stay balanced, focused, and resilient.

Healthy Heart & Mind Tips

Your emotional and physical wellbeing are deeply connected. February is a great time to reflect on that relationship and explore what helps you feel more grounded, energized, and well.

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

Starting March 4, 2026, GreenShield will be transitioning to mandatory receipt uploads for all claims submitted through GreenShield+. This means rather than keeping receipts for future audits, members will be required to upload it during the claim submission, and GS+ will store it securely*. If you are not already doing so, we recommend adopting this practice now.

*All member data is processed/stored within Canada. They use Toronto-based servers that have been audited to meet the highest standards for data security. This includes multiple on-site and off-site encrypted backups, intrusion prevention and detection systems, and various safeguards.

The Customer Contact Centre is currently experiencing elevated wait times due to a seasonal increase in call volume. To help reduce the impact of these high‑volume periods, several initiatives are underway:

Additional mitigation strategies—including overtime, cross‑functional support, and student staffing—continue to be used to help manage peak‑period demand. These combined efforts are intended to stabilize service levels as call volumes return to normal.

An apology is extended for any inconvenience these delays may cause for members.

Members are encouraged to use their GS+ accounts for self‑service options. You can also find answers to any FAQs through the GS+ Help Centre.

January is the perfect time to reflect on the past year and think about what you’d like to accomplish going forward. You can use this fresh start to evaluate your mental health and set emotional goals that truly works for you and your life.

Why it matters:

Your mental well-being influences every part of your life—from relationships and work to physical health. Setting intentional goals can help you feel more balanced and resilient throughout the year.

Ask yourself:

Even modest, consistent efforts can spark positive change!

Set Your Emotional Goal

Website: one.telushealth.com

Username: unitedchurch

Password: eap

Investing in your mental well-being is a gift that lasts all year. Let this be the season to pause, reflect, and grow with intention because new beginnings deserve renewed minds!

*Just a reminder, if you want to access services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Connex is your newsletter that provides information about your pension, benefits, and payroll. If you were previously receiving an email about Connex and didn’t see it in your inbox, check your spam folder! If it’s still not there and you would like to receive Connex, please sign up for the latest news and updates by filling out the form below.

Previous editions can be found in the Connex Archives

Previous editions: