Our thoughts are with all those affected by the ongoing wildfires impacting communities across Canada. These events have resulted in evacuations, disrupted lives, and created uncertainty for many individuals and families.

We recognize that our members and their loved ones may be experiencing stress, anxiety, grief, or other challenges related to these events. If you are struggling or need support, resources are available through both GreenShield and TELUS Health.

Immediate Mental Health Support - Available 24 hours a day, 7 days a week.

GreenShield 24/7 Crisis Line

For immediate mental health support, anyone in Canada can call GreenShield's crisis line to speak directly with a mental health professional.

1-833-707-4747 (English and French)

TELUS Health One

Support is available through the TELUS Health One platform and counselling services.

1-844-671-3327 (English)

1-855-360-5485 (French)

Mental Health and Wellness Online Resources

TELUS Health Employee and Family Assistance Program (EFAP)

Eligible employees and their family members can access a variety of confidential online mental health and wellness resources through the TELUS Health EFAP.

For those affected by wildfires or other emergencies, TELUS Health's Natural Disasters Toolkit provides information and resources to help individuals and families cope with the emotional, practical, and psychological impacts of natural disasters.

You Don't Have to Navigate This Alone

It is normal to experience a range of emotions during emergencies and natural disasters. If you are feeling overwhelmed, anxious, or distressed, please reach out for support. Taking care of your mental health is just as important as taking care of your physical well-being.

We encourage anyone affected by the wildfires to make use of the resources available and to check in with family, friends, colleagues, and neighbours who may also need support.

Reminder

If you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Sleep and recovery aren’t luxuries; they’re essential foundations for brain health and overall well-being. In a world that often glorifies being busy, it’s easy to overlook rest, but quality sleep is what allows your mind and body to reset, recharge, and perform at their best.

Why Sleep Matters

Sleep plays a critical role in:

Memory formation – helping your brain process and store new information

Emotional regulation – supporting resilience and balanced moods

Mental clarity – improving focus, decision-making, and creativity

When we don’t get enough rest, even simple tasks can feel harder, and stress can feel more intense.

Recovery Is More Than Sleep

True recovery includes intentional pauses throughout your day. This might look like:

Taking short breaks to reset your focus

Stepping away from screens

Engaging in calming activities like walking, stretching, or deep breathing

Recovery gives your brain space to recharge—not just overnight, but continuously.

July Moments to Reflect

July 24 – International Self-Care Day

Prioritize habits that support restful sleep, such as setting up a consistent bedtime, limiting screen time before bed, and creating a calming nighttime routine.

July 30 – International Day of Friendship

Strong social connections help reduce stress and improve sleep quality. Reach out to a friend, share a conversation, and nurture the relationships that support your well-being.

Small Steps, Big Impact

This month, challenge yourself to:

Stick to a consistent sleep schedule (even on weekends!)

Create a relaxing wind-down routine

Make time for meaningful connection and self-care

Your brain, body, and overall health will thank you!

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

Annual member statements for the 2025 plan year will be issued to active members of the pension plan at the end of June 2026. If you have not received your statement by the first week of July, please contact pension@united-church.ca to ensure the address on file is correct.

Remember that if you have a spouse, they will automatically receive any pre-retirement death benefit as per pension legislation. However, you should also designate a beneficiary in case your spouse predeceases you. If you do not have a spouse and have not designated a beneficiary, your benefit will go to your estate.

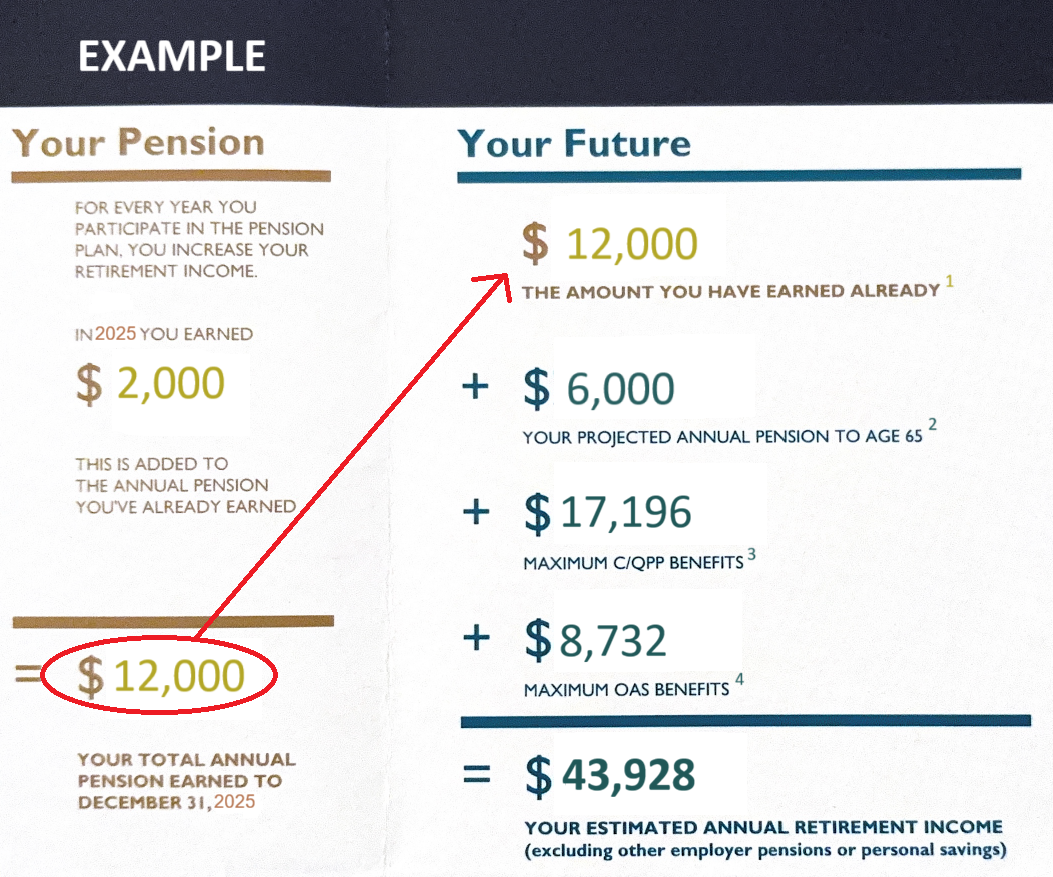

If you have not begun receiving your pension, the statement will contain a box that looks something like this:

1THE AMOUNT YOU HAVE EARNED ALREADY – is calculated based on your pensionable earnings and years of credited service.

2YOUR PROJECTED ANNUAL PENSION TO AGE 65 – is an estimate based on the assumption that you continue working in the same job category until you reach age 65. If you stop working before then, or if your pensionable earnings change, this amount will also change.

3MAXIMUM C/QPP BENEFITS – The amount shown as an example on your pension statement was the maximum amount payable under the Canada Pension Plan in January 2025. Not all Canadians receive the maximum possible payout from the Canada Pension Plan. Please note that the average monthly amount of CPP paid to new recipients (at age 65) in June 2026 is $925.35.

To determine your personal benefit under the Canada Pension Plan, you can request a Personal Access Code (PAC). You can use this code to register for My Service Canada Account, which will provide access to your personal record of contributions and benefits earned under the Canada Pension Plan.

4MAXIMUM OAS BENEFITS – Old Age Security is a pension you can receive if you are 65 years of age or older and have lived in Canada for at least 10 years. The amount you receive depends on your income and how long you lived in Canada or specific countries after the age of 18. If your net income exceeds an income threshold ($95,323 for 2026) you will have to repay some or all of your OAS pension.

When planning for retirement, all of these sources of income, as well as your personal savings and any pension from previous employers, should be considered. We recommend that you consult with a financial planner to help with the financial aspects of your retirement planning.

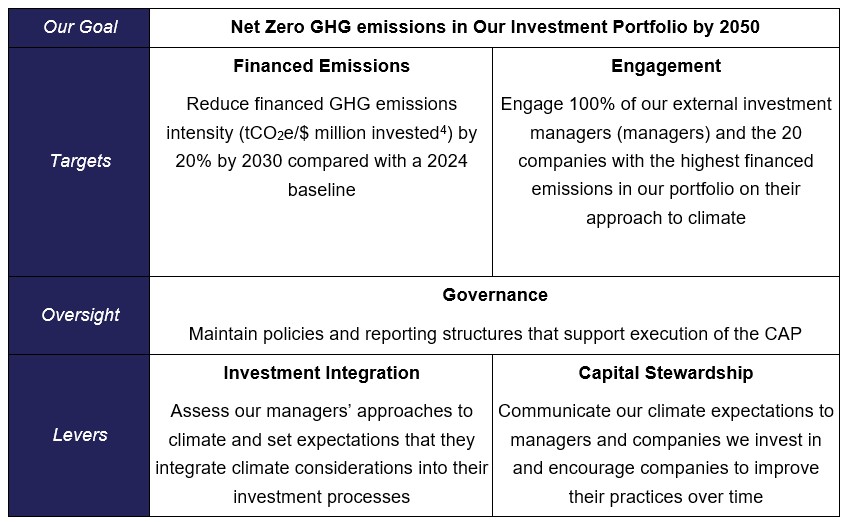

In 2022, the United Church Pension Plan (“the Plan”) committed to achieving net-zero greenhouse gas[3] (GHG) emissions in our investment portfolio by 2050. In December 2025, the Pension Board (“the Board”) approved a Climate Action Plan to operationalize our climate commitment. The Climate Action Plan sets out our climate priorities and commitments and the steps we will take to make progress over time.

Why climate action matters for the pension plan

We recognize that climate change can present risks and opportunities that can affect investment outcomes over time. These risks can take different forms. Physical risks can result from events such as floods, wildfires, or other extreme weather that affect assets, operations, and supply chains. Transition risks can arise as the economy adapts to lower-carbon technologies, policies, and market expectations with consumer demand shifts and regulatory shifts. These changes can affect how companies perform and how investments are valued over time.

As a long-term investor and steward of our members’ financial future, we have a responsibility to manage risks that can influence the value, resilience, and performance of your Plan’s investment over the decades to come.

The Plan’s net-zero by 2050 commitment reflects the scientific consensus on climate change, as well as our fiduciary responsibility to consider factors that may impact our investments. Our Climate Action Plan helps translate that long-term ambition into a structured approach, while building on our existing responsible investment approach and ownership practices.

What is in the Climate Action Plan

The Climate Action Plan is a strategic document that helps explain how we intend to achieve our net-zero commitment.

Our Climate Action Plan sets out key elements of our approach, including:

The Board and Investment Committee oversee the Climate Action Plan. Staff manage day-to-day implementation and work with external investment managers (managers) to advance climate integration, engagement, and reporting. We will review the Climate Action Plan every five years, alongside our strategic planning cycle.

We assess and monitor our managers’ approach to integrating climate considerations into investment decision-making. This includes due diligence during manager selection, annual reviews of climate integration and engagement practices, and ongoing dialogue to better understand climate risks and opportunities across the portfolio.

We engage with managers and portfolio companies to improve practices that reduce climate risk. Our plan commits to engaging all investment managers each year on their approach to climate. This includes discussions on how managers integrate climate into investment processes, what climate targets they have set, how they identify and manage climate-related risks and opportunities, and how they engage companies on climate-related issues.

We also commit to engaging the 20 companies with the highest financed emissions in our portfolio on an annual basis. These discussions may focus on transition planning, emissions reduction, and climate-related disclosure and may occur directly, through investment managers, or through a third-party engagement service provider. This work is also supported through proxy voting at companies’ shareholders meeting.

We track financed emissions in line with guidance from the Partnership for Carbon Accounting for Financials (PCAF) Global GHG Accounting and Reporting Standard, a recognized standard for calculating financed emissions.

As part of our climate action plan, we commit to a 20% reduction in tCO2e per $ million invested by 2030 relative to a 2024 base year in our listed equity and corporate bond portfolios. This target is informed by industry guidance, including the Net-Zero Asset Owner Alliance (NZAOA) Target Setting Protocol.

We recognize that achieving our target will ultimately require the companies we invest in to reduce their GHG emissions. This will depend on a range of factors, such as the availability of new technologies, the overall carbon-intensity of the grid and government policy. If governments and companies do not meet or drop their stated climate targets than it will impact our ability to achieve our financed emissions reduction goals. We also recognize that divestment from high-emitting companies will not reduce real world emissions. We therefore focus our efforts on engaging companies in our portfolio to reduce their emissions. We intend to reassess our financed emissions target every five years.

How members will be kept informed

We aim to provide transparent updates on our progress as we execute against our Climate Action Plan. We will report on our progress through the Responsible Investment Report section of our Annual Report.

Looking ahead

The Climate Action plan is an important step in our ongoing journey. We expect our approach to keep evolving as data improves, guidance develops, and market practice changes. We will remain focused on effectively managing long-term climate risks in support of members’ retirement security. If you have any questions about our Climate Action Plan, please reach out to pensionboard@united-church.ca.

[3] Net-zero refers to a state where the emissions of the companies we invest in are reduced to near-zero with any remaining emissions removed from the air.

[4] This refers to tonnes of carbon dioxide equivalents per million invested.

This June, we’re focusing on connection and community, two essential pillars of social wellbeing. When we take time to build meaningful relationships at work, we create more than just a productive environment—we foster a culture of support, collaboration, and belonging.

In today’s fast-paced and often hybrid workplaces, connection doesn’t always happen by chance. It takes intention. Whether it’s a quick check-in with a colleague, participating in team discussions, or simply taking a moment to listen, these small acts can have a big impact. Strong workplace relationships can boost morale, encourage open communication, and help us feel more engaged and supported in our roles.

Why Connection Matters

Social wellbeing thrives when we feel seen, heard, and valued. A sense of community at work can:

Honoring Pride Month

June is also Pride Month, a time to celebrate and support the 2S and LGBTQIA+ community. It’s an important reminder that true connection starts with inclusion, respect, and authenticity. Creating a workplace where everyone feels safe to be themselves is key to building a strong, connected community.

Pride Month encourages each of us to reflect on how we can contribute to a more inclusive environment, because when we embrace differences and celebrate individuality, we strengthen the fabric of our workplace community.

Small Ways to Build Connection

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

May is Global Mental Health Awareness Month, a time to recognize a crucial truth: mental health isn’t optional—it’s essential. Just as we care for our physical wellbeing, nurturing our mental and emotional health plays a vital role in living a balanced, fulfilling life.

Mental health shapes how we think, feel, relate to others, and handle daily life. By taking care of our mental wellbeing, we build resilience, sharpen our focus and creativity, and nurture stronger relationships. Above all, it’s a reminder that it’s okay to struggle, and reaching out for support is always a valuable step.

Why Mental Health Awareness Matters

Small Actions Can Make a Big Difference

Caring for your mental health doesn’t require major changes. A few simple, everyday habits can help:

Support Is Always Available

Mental health experiences are deeply personal, but no one should have to navigate them alone. If you’re feeling overwhelmed, stressed, or simply not yourself, reaching out for support is a sign of strength. Explore your EFAP, or consider speaking with a mental health professional.

This May (and every month!), let’s continue to create a community where mental health matters. Check in with yourself. Check in with each other. Together, we can foster a healthier, more compassionate workplace for all.

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

The Pension and Benefits Administration System (PABAS) Member Portal is open now through May 15, 2026, allowing you to enter:

Pension beneficiary(ies), and

Life insurance beneficiary(ies) (for benefits eligible members)

You will receive a letter this week from the Benefits Centre with more information about this eBeneficiary campaign and the steps on how to designate your beneficiary(ies).

If you want to get a head start, you can find an electronic copy of the letter below, and step-by-step instructions can be found on the PABAS page of the Benefits Centre website.

If you have any questions, please don’t hesitate to contact us at pabas-go-live@united-church.ca or at 1-855-647-8222.

In our busy day-to-day lives, movement can easily become just another task to check off the list. Mindful movement invites us to slow down and reconnect by being fully present as we move—tuning into our bodies, breathing with intention, and letting go of distractions rather than focusing on performance or outcomes. Practiced this way, physical activity supports not only strength, but also mental health, emotional wellbeing, reduced stress, improved focus, and a greater sense of balance throughout the day.

What does mindful movement look like?

Mindful movement doesn’t have to be complicated or time-consuming. It can include:

Easy ways to integrate it into your routine

Mindful Movement Challenge

Choose one moment each workday to practice mindful movement for five minutes, then pay attention to how your body feels before and after:

At the end of the week, reflect:

Small, mindful moments add up. Just remember, wellness is a journey, not a destination, so keep moving in ways that feel good to you.

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

As part of our ongoing commitment to strengthen the Care Navigation experience, plan members will now see Medical Second Opinion listed under Telemedicine on GreenShield+. This enhancement, introduced on January 1, directs members to a cobranded landing page where they can easily submit a request online. Members who prefer phone support can continue to reach Novus Health directly at 1‑855‑908‑1275 to speak with a Health Information Specialist.

What this means for plan members

Beginning January 1, 2026:

Get answers to your questions

Novus Health’s Medical Second Opinion Program can help you get answers to your questions, such as:

This transition strengthens the long‑term vision for Care Navigation and ensures members continue receiving trusted, high‑quality guidance when navigating important health decisions.

Women’s health evolves in meaningful ways from youth through later adulthood. Each life stage brings its own set of changes - physical, emotional, and hormonal - so in recognition of International Women’s Day on March 8, we’re highlighting the importance of awareness, proactive care and early support for women at every stage of life.

During their lifetime, women may experience shifts in menstrual health, reproductive needs, fertility, mental wellbeing, and later in life, the transition through perimenopause and menopause. Understanding these changes helps women make informed decisions and seek support that reflects their unique needs at each stage.

This month, we’re focusing on awareness around women’s health, with an emphasis on:

Every woman’s journey is different—but access to information, care, and supportive environments can make a significant difference in long-term health and quality of life.

By increasing awareness, we can create space for understanding, empowerment, and healthier outcomes for women at every age.

Just a reminder, if you want to access your EFAP services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap