Annual member statements for the 2025 plan year will be issued to active members of the pension plan at the end of June 2026. If you have not received your statement by the first week of July, please contact pension@united-church.ca to ensure the address on file is correct.

Remember that if you have a spouse, they will automatically receive any pre-retirement death benefit as per pension legislation. However, you should also designate a beneficiary in case your spouse predeceases you. If you do not have a spouse and have not designated a beneficiary, your benefit will go to your estate.

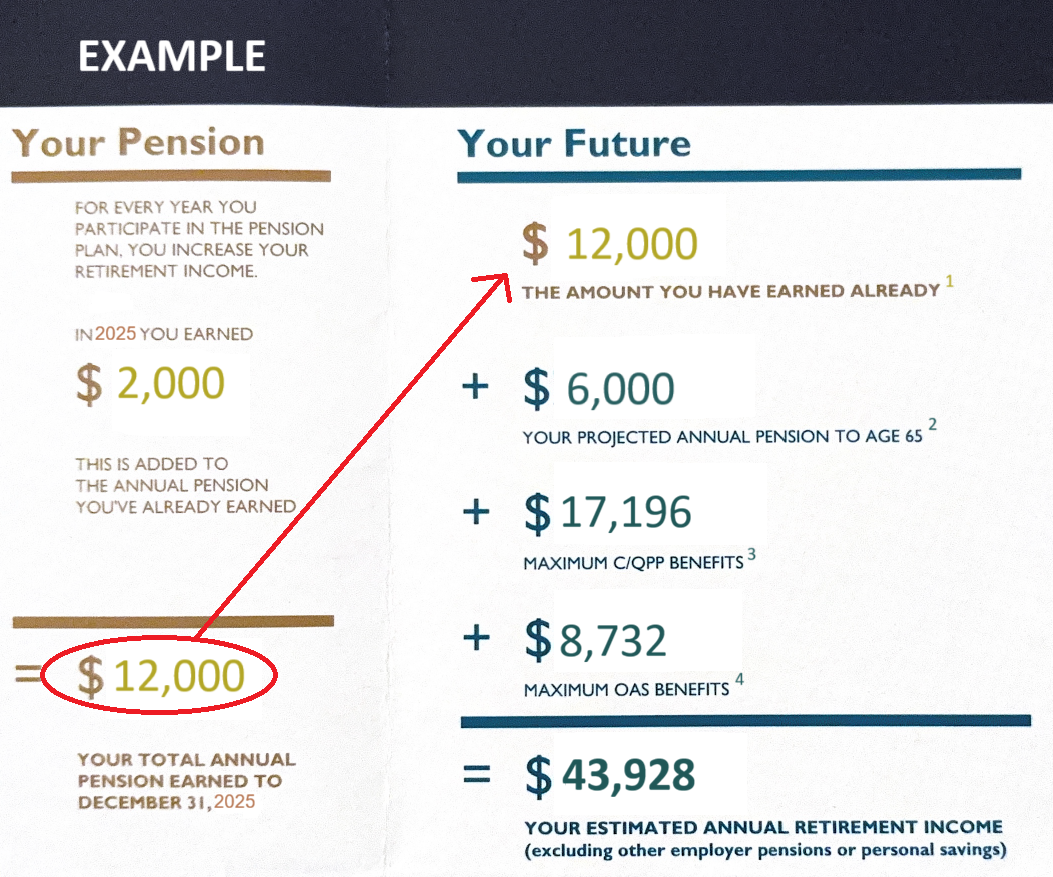

If you have not begun receiving your pension, the statement will contain a box that looks something like this:

1THE AMOUNT YOU HAVE EARNED ALREADY – is calculated based on your pensionable earnings and years of credited service.

2YOUR PROJECTED ANNUAL PENSION TO AGE 65 – is an estimate based on the assumption that you continue working in the same job category until you reach age 65. If you stop working before then, or if your pensionable earnings change, this amount will also change.

3MAXIMUM C/QPP BENEFITS – The amount shown as an example on your pension statement was the maximum amount payable under the Canada Pension Plan in January 2025. Not all Canadians receive the maximum possible payout from the Canada Pension Plan. Please note that the average monthly amount of CPP paid to new recipients (at age 65) in June 2026 is $925.35.

To determine your personal benefit under the Canada Pension Plan, you can request a Personal Access Code (PAC). You can use this code to register for My Service Canada Account, which will provide access to your personal record of contributions and benefits earned under the Canada Pension Plan.

4MAXIMUM OAS BENEFITS – Old Age Security is a pension you can receive if you are 65 years of age or older and have lived in Canada for at least 10 years. The amount you receive depends on your income and how long you lived in Canada or specific countries after the age of 18. If your net income exceeds an income threshold ($95,323 for 2026) you will have to repay some or all of your OAS pension.

When planning for retirement, all of these sources of income, as well as your personal savings and any pension from previous employers, should be considered. We recommend that you consult with a financial planner to help with the financial aspects of your retirement planning.

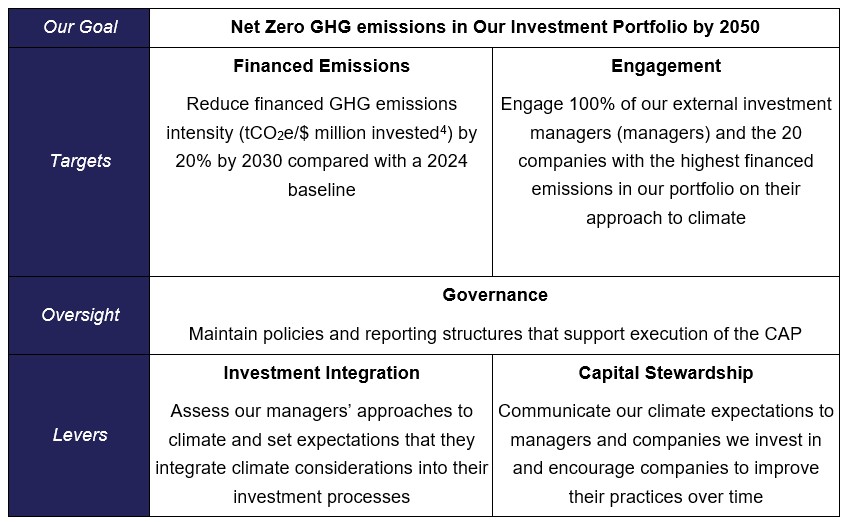

In 2022, the United Church Pension Plan (“the Plan”) committed to achieving net-zero greenhouse gas[3] (GHG) emissions in our investment portfolio by 2050. In December 2025, the Pension Board (“the Board”) approved a Climate Action Plan to operationalize our climate commitment. The Climate Action Plan sets out our climate priorities and commitments and the steps we will take to make progress over time.

Why climate action matters for the pension plan

We recognize that climate change can present risks and opportunities that can affect investment outcomes over time. These risks can take different forms. Physical risks can result from events such as floods, wildfires, or other extreme weather that affect assets, operations, and supply chains. Transition risks can arise as the economy adapts to lower-carbon technologies, policies, and market expectations with consumer demand shifts and regulatory shifts. These changes can affect how companies perform and how investments are valued over time.

As a long-term investor and steward of our members’ financial future, we have a responsibility to manage risks that can influence the value, resilience, and performance of your Plan’s investment over the decades to come.

The Plan’s net-zero by 2050 commitment reflects the scientific consensus on climate change, as well as our fiduciary responsibility to consider factors that may impact our investments. Our Climate Action Plan helps translate that long-term ambition into a structured approach, while building on our existing responsible investment approach and ownership practices.

What is in the Climate Action Plan

The Climate Action Plan is a strategic document that helps explain how we intend to achieve our net-zero commitment.

Our Climate Action Plan sets out key elements of our approach, including:

The Board and Investment Committee oversee the Climate Action Plan. Staff manage day-to-day implementation and work with external investment managers (managers) to advance climate integration, engagement, and reporting. We will review the Climate Action Plan every five years, alongside our strategic planning cycle.

We assess and monitor our managers’ approach to integrating climate considerations into investment decision-making. This includes due diligence during manager selection, annual reviews of climate integration and engagement practices, and ongoing dialogue to better understand climate risks and opportunities across the portfolio.

We engage with managers and portfolio companies to improve practices that reduce climate risk. Our plan commits to engaging all investment managers each year on their approach to climate. This includes discussions on how managers integrate climate into investment processes, what climate targets they have set, how they identify and manage climate-related risks and opportunities, and how they engage companies on climate-related issues.

We also commit to engaging the 20 companies with the highest financed emissions in our portfolio on an annual basis. These discussions may focus on transition planning, emissions reduction, and climate-related disclosure and may occur directly, through investment managers, or through a third-party engagement service provider. This work is also supported through proxy voting at companies’ shareholders meeting.

We track financed emissions in line with guidance from the Partnership for Carbon Accounting for Financials (PCAF) Global GHG Accounting and Reporting Standard, a recognized standard for calculating financed emissions.

As part of our climate action plan, we commit to a 20% reduction in tCO2e per $ million invested by 2030 relative to a 2024 base year in our listed equity and corporate bond portfolios. This target is informed by industry guidance, including the Net-Zero Asset Owner Alliance (NZAOA) Target Setting Protocol.

We recognize that achieving our target will ultimately require the companies we invest in to reduce their GHG emissions. This will depend on a range of factors, such as the availability of new technologies, the overall carbon-intensity of the grid and government policy. If governments and companies do not meet or drop their stated climate targets than it will impact our ability to achieve our financed emissions reduction goals. We also recognize that divestment from high-emitting companies will not reduce real world emissions. We therefore focus our efforts on engaging companies in our portfolio to reduce their emissions. We intend to reassess our financed emissions target every five years.

How members will be kept informed

We aim to provide transparent updates on our progress as we execute against our Climate Action Plan. We will report on our progress through the Responsible Investment Report section of our Annual Report.

Looking ahead

The Climate Action plan is an important step in our ongoing journey. We expect our approach to keep evolving as data improves, guidance develops, and market practice changes. We will remain focused on effectively managing long-term climate risks in support of members’ retirement security. If you have any questions about our Climate Action Plan, please reach out to pensionboard@united-church.ca.

[3] Net-zero refers to a state where the emissions of the companies we invest in are reduced to near-zero with any remaining emissions removed from the air.

[4] This refers to tonnes of carbon dioxide equivalents per million invested.

The Pension and Benefits Administration System (PABAS) Member Portal is open now through May 15, 2026, allowing you to enter:

Pension beneficiary(ies), and

Life insurance beneficiary(ies) (for benefits eligible members)

You will receive a letter this week from the Benefits Centre with more information about this eBeneficiary campaign and the steps on how to designate your beneficiary(ies).

If you want to get a head start, you can find an electronic copy of the letter below, and step-by-step instructions can be found on the PABAS page of the Benefits Centre website.

If you have any questions, please don’t hesitate to contact us at pabas-go-live@united-church.ca or at 1-855-647-8222.

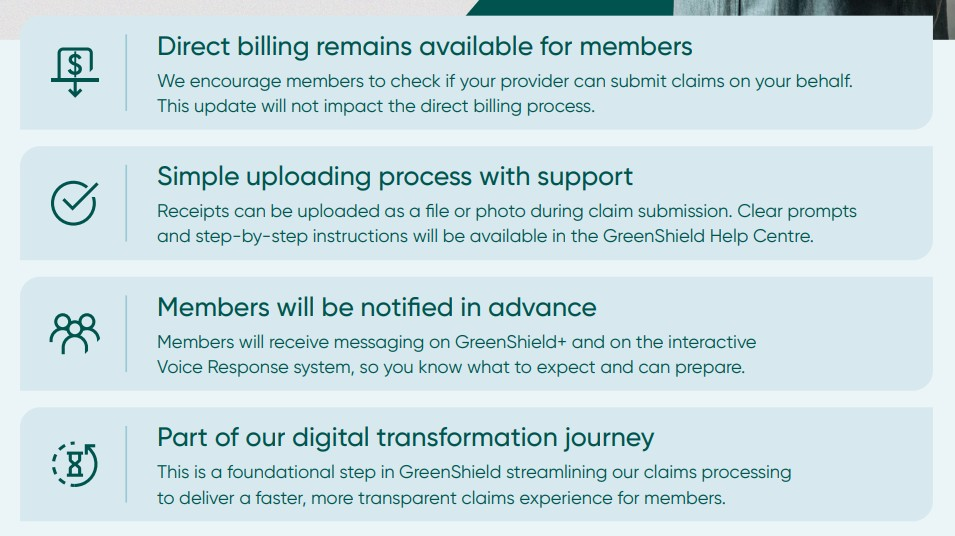

We previously shared that GreenShield would be moving to mandatory receipt uploads for all claims submitted through GreenShield+ starting March 4, 2026. GreenShield has now advised that this transition has been deferred, and there is no new implementation date at this time.

What this means for you:

You can keep submitting claims the same way through GreenShield+, just remember to hold on to your receipts in case they’re needed later.

If you have any questions, please feel free to reach out to the Benefits Team at Benefits@united-church.ca

Starting March 4, 2026, GreenShield will be transitioning to mandatory receipt uploads for all claims submitted through GreenShield+. This means rather than keeping receipts for future audits, members will be required to upload it during the claim submission, and GS+ will store it securely*. If you are not already doing so, we recommend adopting this practice now.

*All member data is processed/stored within Canada. They use Toronto-based servers that have been audited to meet the highest standards for data security. This includes multiple on-site and off-site encrypted backups, intrusion prevention and detection systems, and various safeguards.

Good news! Pension plan members will receive a pension increase effective January 1, 2026.

Pensioners and Deferred Members

Current pensioners and deferred members will receive a 2 percent* increase to their pension amount effective January 1, 2026.

* The Income Tax Act and regulations and the Plan, limit pension increases to the cumulative growth in Consumer Price Index since the pension commenced. For this reason, recently retired pensioners and deferred members who terminated active membership recently may see a lesser increase.

Active Members

For active members, the accrual rate will stay at 1.85 percent in 2026 from the base rate of 1.4 percent. In 2027 the accrual rate is scheduled to return to 1.4 percent.

What Does “Accrual Rate” Mean?

The accrual rate is the rate at which you earn your pension. In 2026, you earn your pension at the rate of x percent of your pensionable earnings.

How Does This Work?

You earn a piece of pension every year that you work and contribute to the plan—like building blocks.

For example, let’s assume that a member’s pensionable earnings stayed constant at $60,000 every year, (for easy figuring). From 2019, that member would earn

|

Year |

Accrual Rate | Formula |

Pension Credit Earned |

|

2019 |

1.4% | 1.4% of $60,000 | $ 840 |

|

2020 |

1.85% | 1.85% of $60,000 | $ 1,110 |

|

2021 |

1.625% | 1.625% of $60,000 |

$ 975 |

| 2022 | 1.85% | 1.85% of $60,000 |

$ 1,110 |

| 2023 | 1.85% | 1.85% of $60,000 |

$ 1,110 |

| 2024 | 1.85% | 1.85% of $60,000 |

$ 1,110 |

| 2025 | 1.85% | 1.85% of $60,000 |

$ 1,110 |

| 2026 | 1.85% | 1.85% of $60,000 |

$ 1,110 |

| 2027 | 1.4% | 1.4% of $60,000 |

$ 840 |

At the end of your career, the annual pension amounts earned each year will add up to the total annual pension you will receive every year for the rest of your life. So, the higher amount earned in 2026 will continue to benefit you for the rest of your retired life.

What about Future Increases?

There is no automatic indexing in our plan. The Pension Board and Pension Plan Advisory Committee annually assess the resources available and determine whether there are surplus funds that can be used to increase benefits.

The holiday season is a time of celebration, but it can also bring added stress and pressure. Between year-end deadlines, family commitments, and financial strain, it’s easy to feel overwhelmed. In December, we’re focusing on two powerful tools to help you navigate the season: gratitude and stress management.

Why Gratitude Matters

Practicing gratitude isn’t just about saying “thank you”—it’s about shifting your perspective. Research shows that gratitude can:

Quick Tip: Start a gratitude list. Each day, write down three things you’re thankful for—big or small. It’s a simple habit that can make a big difference!

Managing Holiday Stress

The holidays can be joyful, but they can also be hectic. Here are a few strategies to keep your stress from sleigh-ing you this season!

The season is about connection and kindness, toward others and yourself, so let’s make space for gratitude and well-being as we close out the year.

Employee and Family Assistance Program (EFAP)

Just a reminder, if you want to access services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account.

Website: one.telushealth.com

Username: unitedchurch

Password: eap

November is a time to reflect on the importance of your mental and physical health. Prioritizing regular screenings, staying active, and taking time to check in with yourself can make a significant difference in your overall wellbeing and vitality. On November 16, it is the International Day for Tolerance. Tolerance begins with listening and creating safe spaces for honest conversations, so let’s embrace empathy, understanding, and support for one another.

Mental health is just as important as physical health, yet many men face unique challenges when it comes to seeking support. Societal expectations and stigma can make it harder to talk about emotional struggles, stress, or anxiety. Mental health affects everything—from your relationships and work performance to your physical health and quality of life.

Ignoring mental health concerns can lead to serious consequences, including increased risk of chronic illness, substance use, and eating disorders. Taking care of your mental wellbeing is a sign of strength, not weakness.

Movember

Movember is dedicated to raising awareness about men’s health issues, including prostate cancer, testicular cancer, and mental health. It’s a reminder to take action, support one another, and speak openly about health concerns.

Take the First Step

Our Employee and Family Assistance Program (EFAP)

We’re excited to share updated access details for our EFAP—a confidential, 24/7 support resource for you and your family. Whether you're navigating personal challenges, seeking financial guidance, or looking for wellness tools, the EFAP is here to support you.

New Access Link: one.telushealth.com

Username: unitedchurch

Password: eap

To access services such as online appointment booking and live chat, you will need to create a personal account. Follow these steps to set up your account. Visit the EFAP portal anytime to explore services, book appointments, or access helpful articles and tools.

Your health matters. Let’s make November a month of action, awareness, and support.

As autumn settles in, many of us notice subtle shifts — in the weather, in our routines, and sometimes, in our mood. October is a powerful time to reflect on mental health, especially with World Mental Health Day observed globally on October 10th. This year’s theme reminds us that mental health is a universal human right, and that includes every one of us.

World Mental Health Day is more than a date on the calendar. It’s a global movement to raise awareness, reduce stigma, and promote access to mental health support. Whether you're thriving, struggling, or somewhere in between, this day is a reminder: your mental health matters.

What’s the Difference?

Signs to Look Out For

If these symptoms resonate with you or someone you know, know that you're not alone. Support is available through our Employee and Family Assistance Program (EFAP), which offers confidential support, counseling, and referrals.

Let’s Normalize the Conversation

Discover how to harness your strengths, express your needs, and build pathways to success by joining Canada Life’s upcoming webinar: Neurodiversity Works – Unlocking the Power of Different Minds in the Workplace. You’ll gain practical tips and strategies to help create inclusive workplaces that support neurodivergent colleagues—either for yourself or your team. The event will be recorded so it can be accessed after the live event on the Workplace Strategies for Mental Health YouTube channel.

Date: October 9, 2025

Time: 1:00 – 2:00 p.m. EDT

Mental health conversations belong in every workplace. By speaking openly, we help create a culture where vulnerability is met with empathy, and seeking help is seen as a strength. Let’s honor World Mental Health Day by continuing to build a workplace where mental health is prioritized, and kindness is part of our culture.

September is here and the back-to-school season begins. Some of us are adjusting to new routines, shifting schedules, and the changing pace of fall–post General Council! If you're a parent managing school drop-offs or simply feeling the seasonal shift, September is a great time to refocus.

Reboot Your Routine

The structure of the school year can help you build healthy habits that support your work-life balance:

Working Parents

Balancing work and family during back-to-school season can be challenging. Here are a few tips to support your well-being:

Just like learning, wellness is a journey, not a destination, so let’s remember to treat ourselves with the same care and encouragement we give to students starting a new year.